A Roth IRA is a retirement savings vehicle that individual taxpayers can establish. The Roth IRA bears many similarities to the traditional IRA and some distinct differences.

Unlike contributions to a traditional IRA, contributions to Roth IRAs are never deductible. Additionally, Roth IRA owners are not subject to the required minimum distribution (RMD) rules, whereas owners of traditional IRAs are subject to the RMD rules. Finally, beneficiaries of both traditional and Roth IRAs are subject to beneficiary RMD rules.

Roth IRAs can be funded through several means, which include:

- Regular contributions

- Rollover contributions

- Roth conversions and

- Recharacterizations

In addition to meeting income/compensation requirements, individuals must meet specific income requirements to utilize some of the funding methods. For example, earnings in a Roth IRA accrue on a tax-deferred basis but are tax-free if certain conditions are met. In some cases, distributions are subject to ordering rules, which determine the source of funding from which the distribution occurs to determine whether the early distribution penalty and income tax apply.

This tutorial explains the key features of Roth IRAs, including operational and compliance requirements.

Who Can Establish and Fund a Roth IRA: Eligibility Requirements

A Roth IRA can be opened (established) by anyone, regardless of age, income, or marital status. The Roth IRA owner must meet the financial institution’s customer identification procedure (CIP) requirements and not be legally prohibited from establishing an account in the US.

However, the funding methods are subject to eligibility requirements and restrictions.

Eligibility for Roth IRA Contributions

An individual must meet the following two requirements to make a Roth IRA contribution:

1. Having Eligible Income or Compensation

An individual can make a regular contribution to a Roth IRA only if he has eligible income/compensation. For this purpose, eligible income/compensation includes

W-2 wages: This includes salaries, wages, tips, bonuses, commissions, and other amounts, usually the amount shown in Box 1 of Form W-2. An exception applies to nontaxable combat pay, which is generally reported in Box 12.

Self-employment income: This income is specifically net earnings from self-employment. This income usually applies to an individual who is a sole proprietor or a partner in a partnership. The income on which contributions can be based is the net earnings from self-employment, generally reduced by (a) the deduction for contributions made to an employer-sponsored plan for the sole proprietor or partner and (b) the deduction for 50% of the individual’s self-employment taxes.

Taxable alimony and separate maintenance: payment received under a divorce decree or separate maintenance arrangement. This income is limited to divorce or separation instruments executed on or before December 31, 2018, that have not been modified to exclude such an amount.

Nontaxable combat pay for members of the US Armed Forces. These amounts are usually reported in Box 12 of Form W-2.

2. Having modified adjusted gross income (MAGI) that does not exceed the limits in effect for the year. See the Roth IRA Contributions Section for details.

Eligibility for Roth IRA Conversions

Before January 1, 2010, an individual was eligible for a Roth IRA Conversion if his MAGI was $100,000 or less and his tax-filing status was not married filing separately. However, these restrictions are repealed effective January 1, 2010.

Eligibility for Rollovers and Transfers

An individual can transfer or rollover balances between Roth IRAs at any time, and such transfers are not subject to any statutory requirements. Rollovers can also occur from qualified plans to Roth IRAs at any time. However, the individual must satisfy the qualified plans’ requirements for making withdrawals from the plan for the rollover.

Only eligible amounts may be rolled over to a Roth IRA

[1] Heroes Earned Retirement Opportunities (HERO) Act of 2006

How to Establish a Roth IRA: Policies and Procedures

The actual procedure for establishing a Roth IRA is determined by the financial institution with which the Roth IRA is established. Many financial institutions allow clients to open IRAs online, including providing any required signature and acknowledgments. Some need the client to print the necessary forms, obtain hard copies, and deliver them to the financial institution via mail or fax. Others require the client to open the IRA in one of their offices face-to-face with a representative.

Regardless of the method used, certain fundamental requirements must be met. In general, the steps for opening or establishing a Roth IRA are as follows:

- Find a financial institution that is approved by the IRS to serve as a custodian or trustee for IRAs

- Complete their required paperwork

- Sign the necessary paperwork and acknowledge receipt of the required disclosures. The Roth IRA is not considered ‘established’, until the owner signs the IRA agreement (plan agreement).

Once these steps have been completed, the Roth IRA can be funded.

Roth IRS Can Only be Opened With Approved Financial Institutions

A Roth IRA must be established with a financial institution approved to be the custodian or trustee of IRAs. Generally, banks and credit unions meet this requirement. Brokerage firms and mutual fund companies generally need to apply to the IRS and can only serve as custodians if they receive approval from the IRS[1]. An individual should not establish a Roth IRA with a financial institution or any other entity unless the financial institution is approved to serve as an IRA custodian or trustee.

Required DocumentationWhen Roth IRA is established

Certain documentation must be provided to the Roth IRA owner by the financial institution which will act as trustee or custodian. In addition, the Roth IRA owner must provide written acknowledgments that the documentation was provided. These documents include the following:

(1) Disclosure statement: The disclosure statement is a two-part document, which must be provided to the Roth IRA owner before the Roth IRA is established[2]. The parts of the disclosure statement include:

I. An explanation of the rules that govern the Roth IRA. These rules include:

- The statutory requirements of the Roth IRA, such as the contribution limits and the consequences of making contributions in excess of the statutory limits

- The Distribution rules, including the tax treatment of Distributions and the Required Minimum Distribution (RMD) rules

- How the owner may revoke the Roth IRA if they wish

- Transactions that could result in penalties. These include using the Roth IRA as collateral for a loan or involving the Roth IRA in a prohibited transaction which could ultimately affect its Tax Exempt status.

- The Portability Rules which apply to the Roth IRA

II. A financial disclosure, which is an explanation of the performance of the investments in the Roth IRA, including where an amount is guaranteed over a period of time, or a projection of growth in the value of the IRA, can reasonably be made. The financial disclosure must show the amount guaranteed or projected to be made available to the benefited individual if:

- Level annual contributions in the amount of $1,000 were made on the first day of each year, and

- The Roth IRA owner was to withdraw the entire amount of the Roth IRA at the end of each of the first five years during which contributions are to be made; at the end of the year in which the benefited individual attains the ages of 60, 65, and 70; and at the end of each year during which the increase in the guaranteed available amount is less than the increase in the guaranteed amount available during any preceding year.

- Similar information must be provided with respect to amounts guaranteed or projected to be made available under a Roth IRA, which is to receive only a rollover contribution, except the amounts guaranteed or projected to be made available are based on only one $1,000 contribution made at the beginning of the year the rollover contribution occurred. [3]

- The actual language to be included in the disclosure depends on the type of investment, where guaranteed, can be reasonably projected, or cannot be either of the foregoing.

Deadline for Providing Disclosure Statement

The disclosure statement must be provided to the Roth IRA owner on the day the Roth IRA is established or earlier.

(2) Plan Agreement: The plan agreement or Roth IRA agreement can be a Roth IRA Custodial Agreement if the IRA is held with a brokerage firm or an IRA Trust Agreement if the Roth IRA is held with a Bank or Trust company. Click here for the IRS’s version of the Custodial IRA Agreement. The Roth IRA Agreement establishes the terms of the Roth IRA, including how much can be contributed to the account, the distribution, rollover, and transfer rules that apply to the Roth IRA, and the types of investments that can be held in the Roth IRA. The agreement should also include information that the Roth IRA is non-forfeitable, cannot be invested in life insurance, must be made in cash- except for rollovers of securities, and that the Roth IRA assets cannot be commingled with other assets. The Roth IRA is ‘established’ when the Roth IRA owner signs the Roth IRA agreement. Custodians and trustees may use the IRS Model Forms for their agreement to use their prototype agreements. Prototype agreements are subject to IRS Approval.

(3) Beneficiary Designation Form: Most Roth IRA Agreements or Roth IRA Adoption Agreements include a built-in Beneficiary Designation Form. Whether incorporated or separate, the Beneficiary Designation Form must be completed by the Roth IRA owner. Failure to complete the Beneficiary Designation Form will result in the beneficiaries of the Roth IRA being determined by the default provisions of the Roth IRA agreement.

Deadline for Establishing a Roth IRA: Technically, there is no deadline by which a Roth IRA must be established. However, if the Roth IRA owner intends to complete a transaction subject to a deadline, the Roth IRA must be established by the deadline to receive the transaction. For instance, if the Roth IRA owner intends to make a regular Roth IRA contribution for last year, the contribution must be made by April 15 this year. As such, the Roth IRA must be established by April 15 of this year.

Right to Revoke a Roth IRA A Roth IRA owner has the right to revoke a Roth IRA within seven days. The seven-day period begins when the Roth IRA owner receives the disclosure statement. However, suppose the disclosure statement is provided to the Roth IRA owner less than seven days before the Roth IRA is established. In that case, the seven-day period begins when the Roth IRA is established[4]. The Roth IRA owner may revoke the Roth IRA by either mailing the instructions, delivering written instructions in person, or by providing the instructions orally. The financial institution can also require that the instructions be provided in both oral and written form. The procedures to which the particular Roth IRA is subject must be explained in the Roth IRA disclosure statement. If the instructions are permitted to be delivered orally, the delivery must be made during the financial institution’s regular business hours. If written notice is required or permitted, the procedure must provide that the instructions are considered mailed on the date of the postmark (or if sent by certified or registered mail, the date of certification or registration) , if it is deposited in the mail in the United States in an envelope or other appropriate wrapper, first-class postage prepaid, and properly addressed.

Entire Balance Must be Returned: When a Roth IRA owner revokes a Roth IRA, the entire balance must be returned to him. The financial institution determines whether any earnings are included with the principal amount. Because of this requirement, some financial institutions will not permit the investment of the assets until the seven-day period has expired.[1] Treas. Reg. 1.408-2(e).[2] Treas. Reg. 1.408-6(d)(4)(ii)(A)(1)[3] Revenue Ruling 86-78[4] Treas. Reg. 1.408-6(d)(4)(ii)(A)(2).

Roth IRA Contributions, Conversions, Rollovers, and Transfers

A Roth IRA can be funded from several sources. These include: Regular Roth IRA contributions, often referred to as Participant Roth IRA Contributions. This includes:

- Spousal IRA contributions.

- Roth IRA conversions from traditional IRAs, SEP IRAs and SIMPLE IRAs

- Rollover contributions from qualified plans, 403(b) plans, and governmental 457(b) plans. These are commonly referred to as Roth Conversions from qualified plans, 403(b) plans, and governmental 457(b) plans.

- Rollover contributions from Designated Roth Accounts

- Transfers and rollovers from other Roth IRAs

Roth IRA Contributions

A regular contribution is deemed to be any monetary additions which an individual makes to his Roth IRA account based on his annual income or compensation. For instance, if an individual earns $50,000 for the year, he may make Roth IRA contributions based on that income.

An individual must meet two requirements in order to be eligible to make a regular Roth IRA contribution. These are:

- The individual must have eligible compensation. For a description of what is considered eligible compensation, see Eligibility for Roth IRA Contributions under Who Can Establish and Fund a Roth IRA: Eligibility Requirements.

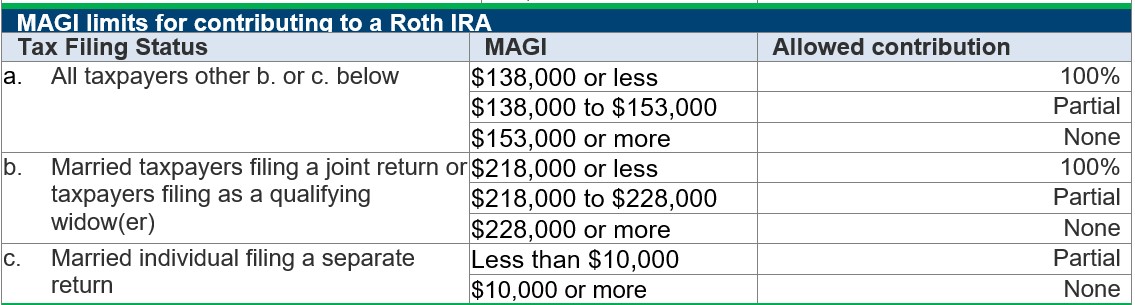

- The individuals modified adjusted gross income (MAGI) must not exceed the following limits:

The following chart also shows the percentage of contributions allowed, when the individual’s MAGI falls into the phase-out range. For 2023, 100% is $7,500 for someone who is at least age 50 by December 31, 2023 and $6,500 for someone is not age 50 by December 31, 2023.

Spousal IRA Contributions

If a married individual has little or no income/compensation, he can still make regular Roth IRA contributions based on the income of his spouse, providing the following requirements are met:

- The couple must file a joint tax return

- The working spouse must have sufficient income or compensation to cover the contribution. If contributions are being made for both spouses, the compensation must be sufficient to cover both contributions

- The contribution to one of the spouse’s Roth IRA cannot exceed the statutory limit in effect for the year. See ‘Contribution Limit’ below

Spousal IRA contributions are-by definition- regular IRA contributions, and as such, are subject to the same rules, regulations and operational & compliance requirements.

Contribution Limit

An individual may contribute up to 100% of eligible compensation to his Roth IRA, providing the contribution does not exceed the limit in effect for the year.

Catch-Up Contributions: Individuals who are at least age 50 by the end of the year can make additional contributions, referred to as catch-up contributions.

Contributions Must Be Made in Cash

Regular Roth IRA contributions must be made in cash[1]. For this purpose, cash includes direct deposits from tax refunds, checks, money orders, and payroll deductions.

Roth IRA Contributions are Not Deductible

Roth IRA contributions are not deductible. Therefore, contributions to a Roth IRA are not affected by an individual’s participation in an employer-sponsored retirement plan. This is unlike the case of a traditional IRA, where an individual’s participation in an employer-sponsored plan could result in the individual being an active participant. The individual’s active participant status could affect his eligibility for taking a deduction for his traditional IRA contribution.

[1] IRC§ 408(a)(1)

Excess Roth IRA Contributions

Excess Roth IRA contribution Defined

An excess Roth IRA contribution is any regular contribution amount in excess of the lesser of the following amounts:

- 100% of the Roth IRA owners taxable income/compensation for the year, or

- the contirbution limit in effect for the year.

Deadline for Removing Roth IRA Excess Contributions

Excess contributions must be removed from the Roth IRA by the Roth IRA owner’s tax filing deadline, including extensions. Individuals who file their tax return on time or file for an extension by the due date of their tax return, receive an automatic six-month extension. For individuals who file on a calendar year, the six-month extension ends on October 15. For instance, if the excess contribution occurred last year, the extension would end on October 15 of this year.

Transactions That Create Excess Contributions

There are several types of transactions that can create excess contributions in a Roth IRA. These include:

Making regular Roth IRA contributions in excess of the contribution limit in effect for the year, as noted above. In some cases individuals mistakenly make contributions to both their traditional IRAs and their Roth IRAs, with the total exceeding the limit in effect for the year. Where someone is eligible to make a contribution of $5,000, that amount can be split between a traditional IRA and a Roth IRA. However, the aggregate contribution to the two IRAs cannot exceed the contribution limit in effect for the year. If the contributions exceed the limit in effect for the year, the excess is applied to the Roth IRA.

Rolling over amounts that are not rollover-eligible. If an amount is rolled over to a Roth IRA, and it is not an eligible rollover distribution, it is treated as a Roth IRA contribution for IRS purposes. This can create an excess contribution in the Roth IRA, if the owner has already made Roth IRA contributions and/or the rollover amount is in excess of the Roth IRA contribution limits for the individual.

Example: John, a 75 year old individual, is required to take an RMD of $10,000 from his traditional IRA. Under the distribution rules, for any year that an individual is required to take an RMD from his IRA, the first distribution which occurs during that year includes the RMD amount. John was unaware that a Roth Conversion is treated as a distribution, and he instructed his IRA custodian to convert $20,000 from his traditional IRA to his Roth IRA.As a result of this error, $10,000 of the $20,000 which was converted to John’s Roth IRA is his RMD for the year. This $10,000 is treated as a Roth IRA contribution, which is in excess of John’s contribution limit. John must remove the excess amount by his tax filing deadline, including extensions in order to avoid the 6% excise tax.

How to Correct a Roth IRA Excess Contribution

There are two primary ways to handle a Roth IRA excess contribution.

(1) Remove the Excess by the Deadline

Removing the excess contribution by the deadline is the only way to avoid the 6% excise tax. For an explanation of the deadline, see Deadline for Removing Roth IRA Excess Contributions earlier.

When the Roth IRA excess contribution is removed by the deadline, it must be accompanied by any net income attributable (NIA) to the excess. If the NIA does not accompany the return of the excess contribution, it is not considered ‘corrected’.If the only credit to the Roth IRA is the excess contribution and the entire amount is being removed, the act of removing the entire balance is sufficient to correct the excess, as that would include the NIA.If only a portion of the contribution is being removed, or if the account has balances attributed to other credits, such as Roth conversions, transfers, or other contributions, the IRS provided formula must be used to determine the NIA. The following is the formula used to compute the NIA:

| NIA | = | Excess | [ adjusted closing balance | – | Adjusted opening balance] |

| Adjusted opening balance |

Let’s look at an example to illustrate how the formula works.John made an excess contribution of $10,000 to his Roth IRA on July 1, at which time his Roth IRA was worth $50,000. Since he had already contributed $6,000 to his Roth IRA for the year, the entire $10,000 is an excess Roth IRA contribution. He had previously made other contributions, conversions and transfers to the same Roth IRA. John submits a request to his Roth IRA custodian to remove the excess from his Roth IRA; at that time, the Roth IRA is valued at $65,000. No other activity occurred during the computation period[2].The NIA is computed as follows:

| NIA | = | Excess | X | [ adjusted closing balance | – | Adjusted opening balance] |

| Adjusted opening balance | ||||||

| NIA | = | $10,000 | X | [ $65,000 | – | $60,000] |

| $60,000 | ||||||

| NIA | = | $10,000 | X | [ $65,000 | – | $60,000] |

| $60,000 | ||||||

| NIA | = | $10,000 | X | $5,000 | ||

| $60,000 | ||||||

| NIA | = | $10,000 | X | -0.08 |

| $833.33 |

Since the NIA is $888.33, the amount that must be removed from John’s Roth IRA to correct the excess contribution is $10,888.33 (excess + the NIA).When NIA is a LossIf the NIA had been a loss, John would reduce the $10,000 by the loss , and remove the net amount.

(2) Remove the Excess After the Deadline

If the excess is removed after the deadline and it is not accompanied by any NIA, John will owe the IRS a 6% excise tax for each year it remains in the Roth IRA as an excess

.Applying Excess to a Future Year

If the excess is not removed by the deadline, it is considered a contribution for the following year. However, unless John is eligible for a contribution for that year and the amount does not exceed his contribution limit, it creates an excess for that year. John will continue to pay the 6% excise tax, until the excess is used up for a future year, or removed from the Roth IRA.

Example:

Assume John’s excess contribution for this year is $5,000. If John does not remove it by October 15 of next year, he will owe the IRS a 6% penalty on the $5,000. The $5,000 will be treated as his Roth IRA contribution for next year, and unless he is eligible for that contribution (for next year); it creates an excess which is subject to the correction procedures explained above.

[1]These limitations are repealed effective January 1, 2010

[2] The period beginning immediately prior to the time that the contribution that is being returned was made to the IRA and ending immediately prior to the removal of the contribution.

Roth IRA Conversions

A Roth IRA conversion is a movement of assets from any of the following accounts to a Roth IRA.

- A traditional IRA

- A SEP IRA

- A SIMPLE IRA. This is permitted only if it has been at least two-years since the first contribution was deposited to the Roth IRA owner’s SIMPLE IRA.

- An account under a qualified plan, 403(b) plan, 403(a) qualified annuity plan, or governmental 457(b) account. In order to convert funds from these accounts to a Roth IRA, the individual must first satisfy requirements to make withdrawals from the account (i.e., experience a triggering event) and the amount must be rollover eligible. The option to convert assets from these accounts to a Roth IRA became effective January 1, 2008[1].

For the purpose of this tutorial, these accounts are referred to as the ‘delivering accounts’.

Roth Conversion Eligibility Requirements

An individual can completed a Roth IRA conversion whether or not she has income/compensation for the year.For Roth conversions that are done before January 1, 2010, the Roth IRA owner must meet the following requirements:

- Have a modified adjusted gross income (MAGI)-or joint MAGI if married- that does not exceed $100,000

- Does not have a tax filing status of married-filing-separately.

These limitations are repealed effective January 1, 2010.No other limitations or eligibility requirements apply to a Roth IRA conversion.

How to Complete a Roth IRA Conversion

A Roth IRA conversion should be completed in accordance with the operational and compliance requirements of the financial institutions (and -if applicable- plan administrator) that are involved in the conversion. In general, a Roth IRA conversion is accomplished as follows:

- The assets are distributed from the delivering account and credited to the Roth IRA. This can occur between accounts held at the same financial institution, or between accounts held at different financial institutions, or

- In the case of a traditional IRA, SEP IRA or SIMPLE IRA that has met the two-year requirement, the account is redesignated as a Roth IRA[2]. In this case, the documentation and operational requirements for opening a new Roth IRA would apply.

The financial institutions involved in the Roth conversion will have documentation and operational requirements that must be satisfied in order for the Roth conversion to be completed.

Indirect Vs Direct Conversions

A Roth IRA Conversion can be accomplished as a direct conversion or as an indirect conversion.

- With an indirect conversion, the funds/assets are paid to the account owner and deposited to the Roth IRA within 60-days of receipt. For tax reporting purposes, the delivery of the assets are treated as a regular distribution. As such, if the delivery is made from a qualified plan, 403(b) account, 403(a) annuity, or a governmental 457(b) account, the payer is required to withhold 20% of the taxable amount for federal taxes.

- With a direct conversion, the funds/assets are paid by the trustee/custodian/plan administrator of the delivering account to the Roth IRA trustee/custodian, and treated for operational and tax-reporting purposes as a direct Roth conversion or a direct rollover contribution. There is no time limit on when the funds must be credited to the Roth IRA.

Whichever method is used, the Roth IRA owner should consult with the parties responsible for delivering and receiving the assets, to ensure that the documentation and operational requirements are satisfied on both sides.

Partial Conversions Permissible

An individual need not convert the entire balance from her delivering account to her Roth IRA. Instead, she can convert a portion of the balance. Partial conversions are often done, instead of full conversions for reasons which include the following:

- The individual cannot afford to pay the tax that would be due on the full conversion

- The individual wants to spread the income from the conversion over several years, and would therefore convert a portion each of that year.

- The individual does not want to move all of the assets into a Roth IRA

If a full conversion was completed and the Roth IRA owner determines that a partial conversion would have been a better option, this can be ‘corrected’ by recharacterizing a portion of the Roth conversion. For an explanation of the recharacterization rules, see

Tutorial: Amounts that Cannot Be Converted to a Roth IRA

An amount can be converted to a Roth IRA, only if the amount is rollover eligible. As such, the following amounts cannot be converted to a Roth IRA.

- Required minimum distribution amounts. If the individual is required to take an RMD from the account for the year, the RMD must be withdrawn before the conversion is completed. If the conversion will be completed as an indirect conversion, the RMD can be included in the amount withdrawn, but the individual must ensure that the amount credited to the Roth IRA does not include the RMD amount.

Example: Johnis 85years old and retired. He plans to convert his 401(k) account balance of $100,000 to his Roth IRA this year. His RMD amount for the year is $4,367. He wants to request a distribution of the entire balance of his 401(k), and instruct the plan administrator to send the amount directly to his Roth IRA custodian, with instructions to deposit the amount to his Roth IRA. John must withdraw the $4,367 before the conversion to the Roth IRA is completed. If he fails to withdraw the RMD amount before the conversion, the $4,367 will create an excess ineligible rollover contribution to his Roth IRA.

- Any of a series of substantially equal distributions paid at least once a year over:

- The participant’s lifetime or life expectancy,

- The joint lives or life expectancies of the participant and his/her beneficiary, or

- A period of 10 years or more,

Hardship distributions, Corrective distributions of excess contributions or excess deferrals, and any income allocable to the excess, or of excess annual additions and any allocable gains A loan treated as a distribution because it does not satisfy certain requirements either when made or later (such as upon default), unless the participant’s accrued benefits are reduced (offset) to repay the loan Dividends on employer securities, and The cost of life insurance coverage.

Tax Treatment of Roth Conversions

A Roth conversion is includible in the Roth IRA owner’s gross income. As such, except for amounts representing after-tax contributions or nondeductible contributions to an IRA, the conversion amount will be taxable.

The 10% early distribution penalty does not apply to a Roth conversion, regardless of the individual’s age at the time the conversion occurs.

Roth conversions are required to be included in the Roth IRA owner’s income for the year the conversion occurs. An exception applies to conversions that are done in 2010. Under this exception, the income from the conversion can be spread over 2011 and 2012 in equal amounts. For instance, if $100,000 was converted in 2010, $50,000 would be added to the Roth IRA owner’s income for 2011 and the balance of $50,000 added to his income for 2012.

Tax Withholding On Conversions

If the conversion is done from a qualified plan, 403(b) plan, 403(a) qualified annuity plan, or governmental 457(b) account, it is not subject to the 20% mandatory withholding that usually applies to taxable amounts that are paid to the account owner. Instead, the plan administrator would withhold zero tax, unless the account owner requests to have taxes withheld.[3]If the conversion is done from a traditional IRA, SEP IRA or SIMPLE IRA, the IRA custodian/trustee is required to withhold 10 % for federal tax, unless the IRA owner request to have no tax withheld.Withheld Amount is Not A ConversionAny amount withheld as tax from a Roth IRA conversion is treated as a regular distribution.

Example:

John request to have the 401(k) balance of $100,000 converted to his Roth IRA. He instructed the plan administrator to withhold 20% for federal tax. As a result only $80,000 was credited to the Roth IRA and 20% was remitted to the IRS as a pre-payment of tax for John.The $20,000 that was withheld for tax is treated as a regular distribution and is subject to income tax and the 10% early distribution penalty on any taxable amount. The 10% early distribution penalty does not apply, if the conversion occurred when John was at least age 59 ½ of if john qualifies for one of the exception to the penalty

Deadline for Completing Roth IRA Conversions

A Roth IRA conversion must be completed by December 31 of a year, in order for it to be treated as a Roth IRA conversion for that year. For this purpose, the effective date of the conversion is the date the assets leave the delivering account. As such, if an individual takes a distribution from a delivering account on December 15, 2023, and the amount is credited to the Roth IRA on January 20, 2024, the transaction is considered to be a 2023-conversion.

[1] IRC § 408A(d)(3)[2] Treas. Reg. 1.408A-2 Q&A 2[3] IRS Notice 2008-30- Q&A-6

Roth IRA Rollovers and Transfers

In addition to regular contributions and conversions, Roth IRAs can be funded via transfers and rollovers. This section explains the rollover and transfer rules that apply to Roth IRAs.

Transfers

A trustee-to-trustee-transfer can occur between two Roth IRAs. There is no limit on the number of times such transfers can occur during any period.When completing a trustee-to-trustee-transfer, the Roth IRA owner should contact the receiving custodian and have them initiate the transfer so as to reduce the chances of errors occurring. The receiving custodian will generally have the Roth IRA owner complete paperwork to indicate whether the assets must be transferred in-kind, or if non-cash assets must be liquidated and then transferred.A transfer is a non-reportable and nontaxable transaction

Rollovers Between Roth IRAs

A rollover between two Roth IRAs occurs when the Roth IRA owner takes a distribution from one Roth IRA and does a rollover of the amount (or a portion of it) to another Roth IRA as a rollover contribution. Such a rollover is subject to the following rules:oThe same property that was distributed must be rolled overoThe rollover must be completed within 60-days of the Roth IRA owner receiving the distributionoA Roth IRA cannot be involved in a rollover more than once during a 12-month period.Rollovers between Roth IRAs are reportable, but are nontaxable.

From a Traditional IRA, SEP IRA or SIMPLE IRA to a Roth IRA

A rollover from a traditional IRA, SEP-IRA or SIMPLE IRA to a Roth IRA is considered a Roth IRA conversion. The credit to the Roth IRA should be treated as a ‘conversion’ for tax reporting purposes, and not as a regular rollover contribution.For conversions done before January 1, 2010, the Roth IRA owner must meet the following two requirements:

Have a modified adjusted gross income (MAGI) or $100,000 or less, and

Tax filing status must not be married-filing-separately these limitations are repealed for conversions that occur January 1, 2010 and after.Conversions are reportable and (except for amounts representing after-tax amounts) are taxable to the Roth IRA owner for the year the conversion occurs. There are no limits on the number of times these conversions can occur during any given period. However, in the case of a reconversion, there is a restriction on the time period within which it can occur. For an explanation of these restrictions, see Tutorial: Roth IRA Reconversions.

For more on the Roth IRA conversion rules, see Tutorial: Roth IRA Conversions.

From a qualified plan, 403(b), 403(a) or governmental 457(b) plan

A rollover from a qualified plan, 403(b) , 403(a) or governmental 457 (b) plans is considered a qualified rollover contribution or Roth conversion. These can be done as direct conversions or indirect conversions. Similar to conversions from traditional IRAs, SEP IRAs and SIMPLE IRAs, the Roth IRA owner is subject to MAGI and tax-filing status limitations, which are repealed effective January 1, 2010.

The individual must be eligible to make withdrawals from these plans in order for the rollover/conversion to occur and the amount must be rollover eligible in order to be credited to the Roth IRA.

If the conversion is done as an indirect conversion, the amount must be credited to the Roth IRA within 60-days of the Roth IRA owner receiving the assets.There is no limit on the number of times these transactions can occur

From a Designated Roth Account

A rollover from a designated Roth Account (DRA)– also know as Roth 401(k)s and Roth 403(b)s, can be made to a Roth IRA, providing the Roth IRA owner is eligible to make withdrawals from the DRA. Similar to rollovers from qualified plans, there is no limit on the number of times a rollover can occur from a DRA to a Roth IRA.From Roth IRAs to Other Types of Retirement Plans

Assets cannot be rolled-over or transferred from a Roth IRA to any other type of retirement plan. The only permitted movement of funds/assets from a Roth IRA to another type of retirement plan is recharacterizations. These are:

- A recharacterization of an IRA contribution from a Roth IRA to a traditional IRA

- A recharacterization of a Roth conversion that was made from a traditional IRA, SEP IRA or SIMPLE IRA

- A recharacterization of a Roth conversion that was made from a qualified plan, 403(b) account, 403(a) annuity, or governmental 457(b) plan

Roth IRA Recharacterizations

Important: The Tax Cuts and Jobs Act of 2017 repealed the option to recharacterize Roth conversions, for Roth conversions done after 2017. As such, only regular contributions to traditional IRAs and Roth IRAs may now be recharacterized.

============================================

A recharacterization is either a reversal of a Roth IRA conversion or changing a contribution from a Roth IRA to a traditional IRA or from a traditional IRA to a Roth IRA. A recharacterization is usually done for reasons which include the following:

Recharacterizations of Contributions

The individual made the contribution to a Roth IRA and it is determined that he is ineligible for the Roth IRA contribution

An individual made a contribution to a traditional IRA and is ineligible to claim the deduction, but is eligible for a Roth IRA contribution

The individual decides that it makes better financial sense to fund the other type of IRA, instead of the one that was initially funded with the contribution

An individual who made a regular contributions to one type of IRA (Roth IRA or traditional IRA), and wants to change the type of IRA to which the contribution was made, for personal, eligibility or tax reasons.

Recharacterizations of Roth IRA ConversionsoThe Roth IRA owner is ineligible for the conversion

The conversion is a reconversion that was done before the amount was eligible to be reconverted. See Tutorial: Roth IRA Reconversions for an explanation of the reconversion rules

The value of the assets has fallen much lower than they were at the time the conversion occurred.oThe individual decides that it makes better financial sense to keep the assets in a traditional IRAoThe individual is unable to pay the tax that would be due on the conversion

Deadline for Completing a Recharacterization Recharacterizations must be completed by the IRA owner’s tax filing deadline, including extensions. Individuals who file their tax return on time or file for an extension by the due date of their tax return, receive an automatic six-month extension. For individuals who file on a calendar year, the six-month extension ends on October 15. For instance, if the excess contribution occurred last year, the extension would end on October 15 of this year.

How to Recharacterize a Contribution or Roth ConversionWhen an IRA contribution or a Roth IRA conversion is recharacterized, it must be accompanied by any net income attributable (NIA) to the excess.

If the only credit to the Roth IRA is the excess contribution or the Roth conversion that is being recharacterized, recharacterizing the entire balance is sufficient.

If only a portion of the contribution or Roth conversion is being recharacterized, or if the account has balances attributed to other credits, such as other Roth conversions, transfers, or other contributions, the IRS provided formula must be used to determine the NIA. The following is the formula used to compute the NIA:

| NIA | = | Contribution or conversion | [ adjusted closing balance | – | Adjusted opening balance] |

| Adjusted opening balance |

Let’s look at an example to illustrate how the formula works.John made a conversion of $10,000 to his Roth IRA on July 1, at which time his Roth IRA was worth $50,000. John no longer wants to pay the tax on the conversion and decides to recharacterize the amount by the deadline. He had previously made other contributions, conversions and transfers to the same Roth IRA. John submits a request to his Roth IRA custodian to remove the excess from his Roth IRA; at that time, the Roth IRA is valued at $65,000. No other activity occurred during the computation period[1].The NIA is computed as follows:

| NIA | = | Conversion amount | X | [ adjusted closing balance | – | Adjusted opening balance] |

| Adjusted opening balance | ||||||

| NIA | = | $10,000 | X | [ $65,000 | – | $60,000] |

| $60,000 | ||||||

| NIA | = | $10,000 | X | [ $65,000 | – | $60,000] |

| $60,000 | ||||||

| NIA | = | $10,000 | X | -$5,000 | ||

| $60,000 | ||||||

| NIA | = | $10,000 | X | -0.08 | ||

| $833.33 |

Since the NIA is $888.33, the amount that must be recharacterized from John’s Roth IRA to is $10,888.33 (excess + the NIA).When NIA is a LossIf the NIA had been a loss, John would reduce the $10,000 by the loss, and recharacterize the net amount.

[1] The period beginning immediately prior to the time that the contribution that is being returned was made to the IRA and ending immediately prior to the removal of the contribution.

Roth IRA Distributions

Distributions from Roth IRAs are tax and penalty-free, if the distribution is qualified. For non-qualified distributions, the ordering rules must be used to determine if tax and/or the early distribution penalty applies to the distribution amount.

Qualified Distributions DefinedA qualified Roth IRA distribution is one that meets the following two requirements:

It occurs at least five years after the owner established and funded her first Roth IRA and

It occurs under one of the following circumstances:

After the Roth IRA owner reaches age 59 ½,oThe distribution was used towards the purchase, building or rebuilding the first home for an eligible party. This is subject to a life-time limit of $10,000,

The distribution occurs after the owner is disabled or

The distribution was made by the Roth IRA owner’s beneficiaries after the owner’s death.

A distribution that meets these two requirements is tax free and is not subject to the early distribution penalty.

Non-Qualified Distributions: For distributions that are non-qualified, the ordering rules must be used to determine whether the amount is subject to income tax and/or the 10% early distribution penalty.

According to these ordering rules, distributions from Roth IRAs occur in the following order:

1.Regular Roth IRA contributions: Distribution of these amounts are always tax and penalty free , and can be taken at anytime- regardless of the length of period for which they were held in the Roth IRA.

2.Roth conversion amounts: These are distributed only after all regular contributions have been distributed from the Roth IRA. These are subject to a 10% early distribution penalty, if it has been less than five years since the amount was converted, unless an exception applies. However, no income tax applies, as these amounts would have already been taxed at the time of conversion. Each conversion is subject to its own five year holding period. Therefore, if the owner converted amounts in different years, the earlier conversions are withdrawn first. For instance, if an individual converted amounts in 2023 and 2024, the 2023 conversions are withdrawn before the 2024 conversions. Further, for each conversion amount, any taxable portion is withdrawn before non-taxable amounts

Example 1:

Jane converted $50,000 to her Roth IRA in 2024. In 2028, she converted an additional $40,000. Jane takes a distribution of $20,000 from her Roth IRA in 2029. The distribution is free from federal tax, because the tax was paid when she filed her 2024 tax return. It is also penalty-free because it is considered distributed from the $50,000 under the ordering rules, and the $50,000 has aged for at least five years.3.

Earnings: These amounts are distributed only after all regular contributions and conversion amounts have been distributed. These amounts are subject to income tax. They are also subject to the 10% early distribution penalty, unless an exception applies The exceptions to the 10% early distribution penalty applies to amounts used for (or as a result of ) the following:

Unreimbursed medical expenses that are more than 7.5% of the owner’s adjusted gross income

The distributions are not more than the cost of the owner’s medical insurance

The distributions occurred while the owner is disabled

The distribution was made from an inherited IRA

The distribution is part of a substantially equal periodic payment (SEPP)

The distributions are not more than the qualified higher education expenses of an eligible party

The distribution was used to buy, build, or rebuild a first home for the Roth IRA owner or a qualifying family member

The distribution is due to an IRS levy of the IRA

The distribution represents any nontaxable amount from the IRA. Nontaxable amounts would be from any non-deductible contributions or rollover of after-tax amounts that was converted to the Roth IRA, or from regular contributions made to the Roth IRA

The distribution was eligible for rollover and is rolled over within the 60-day period

For purposes of determining whether a Roth IRA distribution is qualified, all of an individual’s ‘own’ Roth IRAs are treated as one Roth IRA. That is, this does not include inherited Roth IRAs.

RMD Rules and Beneficiary Options

Unlike traditional IRAs, the required minimum distribution (RMD) rules do not apply to Roth IRA owners. They do, however, apply to Roth IRA beneficiaries. The following is a high-level summary of the distribution options for the beneficiary of a Roth IRA.

Because Roth IRA owners are not subject to RMDs, the distribution options available to the beneficiary of a Roth IRA are the same, regardless of the age at which the owner dies. So, for instance, if a Roth IRA owner dies at 50 or 80, the distribution options are the same for the beneficiary. This is unlike those that apply to a traditional IRA, for which the distribution options depend on whether the owner died before the required beginning date.

The following is a high-level summary of the distribution options for the beneficiary of a Roth IRA:

- If the beneficiary is not a designated beneficiary

If the Roth IRA beneficiary is not a designated beneficiary, the 5-year rule applies. Under this rule, distributions are optional until the 5th year that follows the year of the Roth IRA owner’s death, at which time the entire balance must be distributed

- If the beneficiary is a designated beneficiary

If the Roth IRA beneficiary is a designated beneficiary, the 10-year rule applies. Under this rule, distributions are optional until the 10th year that follows the year of the Roth IRA owner’s death, at which time the entire balance must be distributed

- If the beneficiary is an eligible designated beneficiary

If the Roth IRA beneficiary is an eligible designated beneficiary, the beneficiary may choose between (a) the 10-year rule or (b) taking distributions over their life expectancy. These life expectancy distributions must begin by December 31 of the year after the year the Roth IRA owner dies.

Roth IRA Summary

- Roth IRAs can be established by anyone. However, only eligible individuals can make regular Roth IRA contributions

- Custodians are subject to certain disclosure requirements when they establish Roth IRAs for clients. Failure to meet these requirements can result in a breach of compliance

- For conversions that occur before January 1, 2010, individuals must have a MAGI of $100,000 or less and cannot file as ‘married-filing-separately.

- Roth IRAs are subject to rollover and transfer rules that are similar to those that apply to traditional IRAs.

- Contributions in excess of the statutory limit can result in the Roth IRA owner owing the IRS penalties, unless the excess is timely corrected.

- Amounts that are converted and subsequently recharacterized cannot be reconverted before a predefined period.

- Distributions may be subject to income tax and or early distribution penalties, unless certain requirements are satisfied.

Sources

- IRC §408A

- TD 8816- Final Roth IRA Regulations

- IRS Publication 590a

- IRS Publication 590b